When I first learned about the FHA loan, I realized it could help people like me and maybe you too buy a home with as little as 3.5% down. That means if you’re looking at a $250,000 USD home, you could get started with just $8,750 USD. That’s a huge difference compared to the 20% down payment many traditional loans require, which would be $50,000 USD on the same house.

One of the benefits of FHA home loans is that their requirement include a low minimum credit score to apply for a loan and also down payments better than other conventional loans. The service is very popular among first-time homebuyers.

What is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD). This insurance protects lenders, allowing them to offer mortgages to borrowers with lower credit scores and smaller down payments. In essence, the FHA reduces the lender’s risk, making homeownership more accessible.

Let me give you an example: I applied for an FHA loan for a $200,000 USD home. Instead of needing a $40,000 USD down payment (which I didn’t have), I only had to come up with $7,000 USD. That made homeownership feel reachable, not just a dream.

How Does FHA Loans Work?

First of all, an FHA loan is a mortgage service offered or insured by Federal Housing Administration. While Federal Housing Administration (FHA) is a government program set to offer you mortgages. They connect you with borrowers who are willing to finance your home with benefits such as down payments as low as 3.5%.

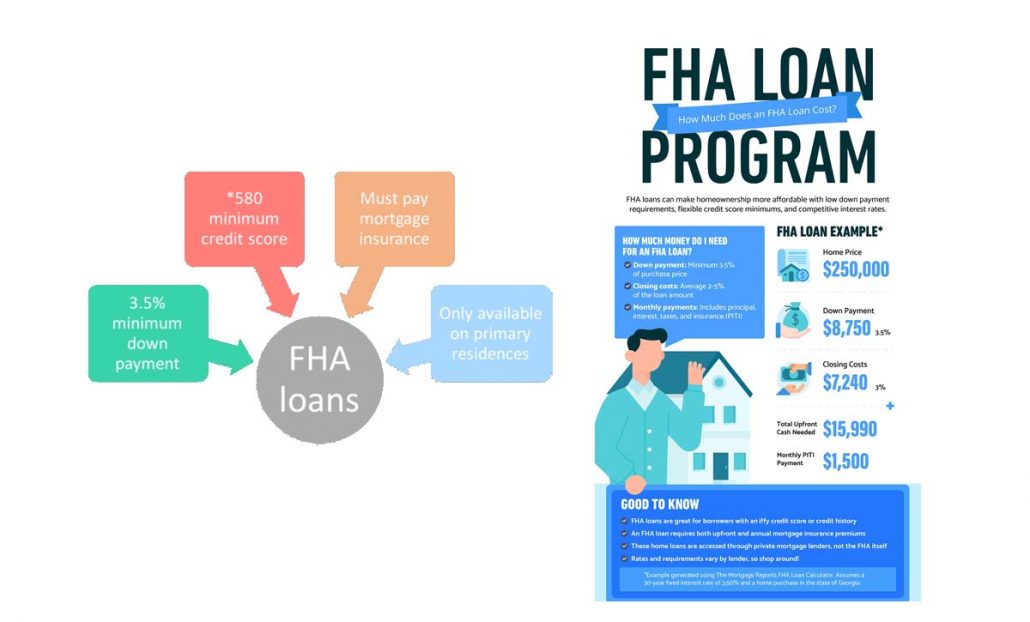

FHA loans offer 15- and 30-year terms with an amazing fixed interest rate. FHA agency comes with a flexible underwriting standard suitable for borrowers who do not have pristine credit or a high income to become a homeowner. The important thing is that a borrower must pay FHA mortgage insurance. They ensure that lenders are protected against loss if you default on the loan. Mortgage insurance is often requested when borrowers decide to offer less than 20%.

According to reports from Bankrate.com, All FHA loans require the borrowers to pay two mortgage insurance premiums. This includes Upfront mortgage insurance premiums and Annual mortgage insurance premiums.

Benefits of FHA Loans

FHA loans, insured by the Federal Housing Administration, are designed to make homeownership more accessible, particularly for first-time homebuyers and those with limited financial resources. Here’s a breakdown of their key benefits:

- Lower Down Payment Requirements: One of the most significant advantages is the ability to put down as little as 3.5% of the home’s purchase price, if you have a credit score of 580 or higher. This makes homeownership attainable for those who haven’t saved a large sum of money.

- More Lenient Credit Requirements: FHA loans are more forgiving when it comes to credit scores compared to conventional loans. This can be a lifeline for individuals with less-than-perfect credit histories.

- Flexible Debt-to-Income (DTI) Ratios: FHA loans typically allow for higher DTI ratios, meaning you can qualify even with more existing debt. This can be helpful for those with student loans or other financial obligations.

- Assumability: In some cases, FHA loans can be assumed by a buyer, which could be a valuable selling point if interest rates rise. This allows a buyer to potentially take over your existing loan with its current interest rate.

- Help for First-Time Homebuyers: FHA loans are very popular with first time home buyers, because of the easier qualifications.

It’s important to note that FHA loans also come with certain requirements, such as mortgage insurance premiums (MIP), which protect the lender in case of default. However, for many, the benefits of FHA loans outweigh the costs, making them a valuable tool for achieving homeownership.

Is An FHA Loan Right For You?

Yes, FHA loans are right for you because with offer you a down payment as low as 3.5%, and you can acquire a loan even with a low credit score. FHA loans are very suitable for acquiring a mortgage loan and it good option for first-time homebuyers who don’t have enough money for a large down payment. The interesting aspect of FHA loans is that borrowers who suffer from bankruptcy or foreclosure can qualify for FHA-backed mortgages.

How Much Can You Borrow with an FHA Loan?

The loan limits vary by county, but in most areas, the limit for a single-family home is around $498,257 USD in 2025. In high-cost areas like California or New York, it can go as high as $1,149,825 USD.

Let’s say you’re house-hunting in a place like Dallas. The FHA limit there might be around $500,000 USD. That means you could buy a home for that amount with just 3.5% down about $17,500 USD. When I was house shopping, that made me feel like I had real options, not just fixer-uppers.

Required Qualification for an FHA Loan

There is a certain qualification for an FHA loan. However, for you to be approved for an FHA loan, you must meet the following qualifications:

- A FICO score of 500 to 579, plus a 10 percent down payment.

- You must possess a verified employment history for at least two years.

- You must have a verified income via pay stubs, and others.

- Use the loan to finance a primary residence.

- The property must follow the required FHA-approved appraiser and also HUD guidelines.

- You must have a front-end-debt ratio.

- You must have a back-end debt ratio.

In addition, for borrowers with bankruptcy issues, the period of application is one to two years after bankruptcy while for foreclosure, three years.

Understanding Mortgage Insurance Premiums (MIP)

MIP is a critical component of FHA loans. It consists of two parts:

Upfront Mortgage Insurance Premium (UFMIP): Paid at closing, this is typically 1.75% of the loan amount.

Annual Mortgage Insurance Premium (Annual MIP): Paid monthly, the amount varies based on your loan amount, loan term, and loan-to-value ratio.

How to Locate an FNA Lender and Apply for an FHA Loan

You can acquire your home loan from FHA-approved lenders which offer different rates, costs, and underwriting standards. Also, you can get FHA loans from different sources which include large banks, credit unions, and independent mortgage lenders.

Application to Apply for FHA Loans

Know your budget

First of all, you need to understand your budget before you can apply. This will better help you to understand the amount you can afford to purchase your dream home. Make use of the following important factors such as your current income, expenses, and savings to calculate your budget. Likewise, you can make use of the Bankrate mortgage calculator to calculate the monthly payment.

Compile your documents:

If you want to borrow a huge sum of money, this means you’ll be handing over a complete look at your total finances. However, before you apply for FHA loans, you need to provide the following documents, two years of tax returns, two recent pay stubs, a driver’s license, full statements of your assets, and other important documents.

Compare your offers

Lastly, before you apply for an FHA loan, you can compare various offers or get pre-approved with different lenders. This will help you to compare the various rates offers and terms to get a suitable deal.

To find out more information on FHA vs conventional loans, FHA loan limits in 2021, and also other types of FHA loans like 203(k), HECM, Energy Efficient Mortgage, and 245(a) loans, you can visit Bankrate.com.

Mortgage Insurance and Costs

Here’s the part I wish someone had explained to me better: FHA loans require two types of mortgage insurance:

- Upfront Mortgage Insurance Premium (UFMIP) – usually 1.75% of the loan. On a $250,000 USD loan, that’s $4,375.

- Annual Mortgage Insurance Premium (MIP) – typically 0.55% to 1.05% of your loan amount, paid monthly.

For my $200,000 USD loan, my monthly MIP came out to around $117 USD. Not cheap, but manageable, and worth it to own a home

FHA Loan Limits

FHA loan limits vary by county and are based on the median home prices in those areas. You can find the current FHA loan limits on the HUD website.

FHA 203(k) Loans

For those looking to purchase and renovate a fixer-upper, the FHA 203(k) loan is an excellent option. It allows you to finance both the purchase and renovation costs into a single loan.

Refinancing with an FHA Loan

FHA loans can also be used for refinancing. The FHA Streamline Refinance program offers a simplified process for homeowners with existing FHA loans to lower their interest rates.

FAQ’s

What is the minimum credit score required for an FHA loan?

The minimum credit score is 500, but a score of 580 or higher allows for a 3.5% down payment.

Can I use gift funds for my FHA down payment?

Yes, you can use gift funds from family or friends.

What is MIP?

MIP stands for Mortgage Insurance Premium. It protects the lender in case of default and is required for FHA loans.

Are FHA loans only for first-time homebuyers?

No, FHA loans are available to both first-time and repeat homebuyers.

What is the maximum loan amount for an FHA loan?

FHA loan limits vary by county and are based on median home prices.

Can I refinance my existing FHA loan?

Yes, you can refinance using the FHA Streamline Refinance program.

What is an FHA 203(k) loan?

An FHA 203(k) loan allows you to finance both the purchase and renovation costs of a fixer-upper into a single loan.

How do I find an FHA-approved lender?

You can find FHA-approved lenders by searching online or asking your real estate agent for recommendations.

What documents do I need for an FHA loan application?

You’ll need documents such as proof of income, tax returns, bank statements, and credit reports.

How long does the FHA loan process take?

The process can take anywhere from 30 to 45 days, depending on various factors.