What is a Home Equity Line of Credit?

What does a home equity line of credit or HELOC mean? In the articles, you can learn more about home equity of credit or HELOC. In the meantime, a home equity line of credit known as HELOC is a term that enables you to borrow money that complies with the value of your home to access cash as needed. HELOC or home equity line of credit is another type of mortgage that offers you money or allows you to borrow money based on the value of your home.

This enables you to benefit from your home equity line of credit where you can repay all or some monthly, this is similar to a credit card. HELOC allows you to borrow money against your equity. It is calculated by subtracting the home value from the amount owed on your mortgage. If you own your home outright this provide more advantage to get a HELCO.

How Does a HELCO Work?

Similar to a credit card which enables you to borrow money even with a low spending limit. As for the home equity line of credit, the offers you a flexible way to borrow money against your home equity, repay and repeat. Keep in mind, that you need to know that HELOC interest rates are adjustable, meaning that the interest rate can go up and down. Therefore, the interest rate on HELOC will be adjustable as well.

However, to set up your rate, the lender first begins with an index rate, and afterward adds a markup based on your credit profile. Based on statistics, a high credit score tends to lower your markup. The markup can also be called the margin. This is more of the reason why you need to see the amount before signing up for HELOC.

Benefits of HELOCs

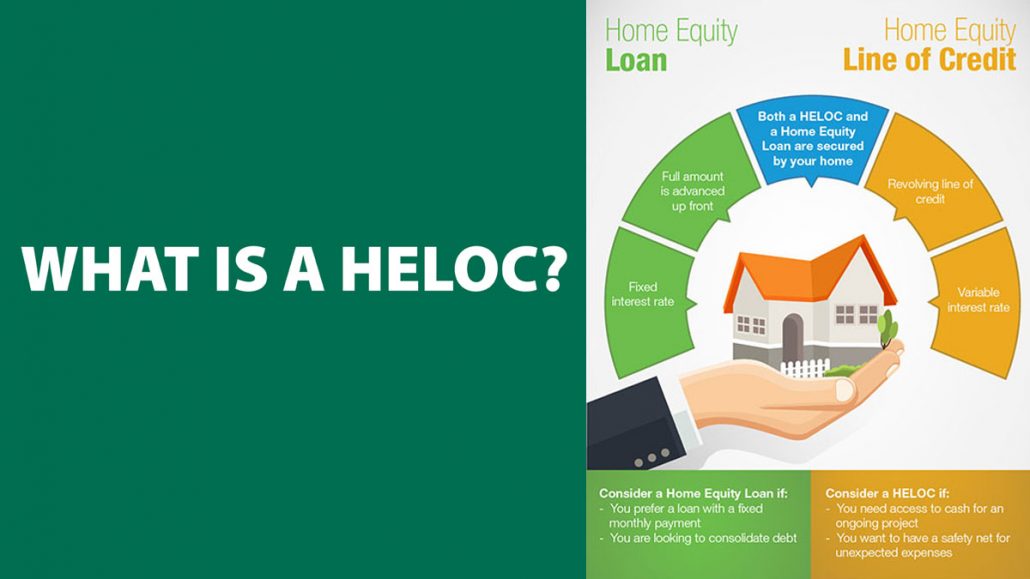

- Flexibility: HELOCs offer flexibility in accessing funds as needed, unlike home equity loans that provide a lump sum upfront.

- Lower Interest Rates: HELOCs often have lower interest rates compared to other types of loans, such as personal loans.

- Tax Deductions: Interest paid on HELOCs used for substantial home improvements may be tax-deductible.

- No Prepayment Penalties: HELOCs typically don’t have prepayment penalties, allowing you to pay off the balance early without incurring extra fees.

HELOC Requirements and Qualifications

Here are the general requirements and qualifications for obtaining a Home Equity Line of Credit (HELOC):

- Equity in your home: You’ll need a certain amount of equity in your home, typically at least 15-20%. This is the difference between your home’s value and the amount you owe on your mortgage.

- Good credit score: A good credit score is essential, as it demonstrates your ability to repay the loan. Most lenders prefer a score of 680 or higher.

- Low debt-to-income (DTI) ratio: Your DTI ratio, which compares your monthly debt payments to your gross monthly income, should be low. Lenders generally prefer a DTI ratio of 43% or lower.

- Stable income: You’ll need to demonstrate a stable and reliable income source to ensure you can make the monthly payments.

- Appraisal: The lender will likely require an appraisal of your home to determine its current market value.

- Other factors: Lenders may also consider other factors, such as your employment history, the age and condition of your home, and the overall economic climate.

It’s important to note that these are general guidelines, and specific requirements may vary depending on the lender and your individual circumstances.

HELOC Rates and Fees

Here are the typical rates and fees associated with a Home Equity Line of Credit (HELOC):

Interest rates: HELOCs typically have variable interest rates, meaning they can fluctuate based on the prime rate or another benchmark. Some lenders may offer an introductory fixed rate for a limited time, which then converts to a variable rate.

Annual fees: Some lenders charge an annual fee, typically ranging from $50 to $100, to maintain the HELOC account.

Transaction fees: Some lenders may charge fees for each transaction or withdrawal you make from the HELOC.

Early closure fees: If you close the HELOC account within a certain period, typically one to three years, some lenders may charge an early closure fee to recoup their closing costs.

Appraisal fees: Lenders typically require an appraisal to determine the current market value of your home, and you’ll be responsible for paying the appraisal fee.

Other fees: Other potential fees may include application fees, origination fees, and recording fees.

It’s essential to compare rates and fees from multiple lenders to find the most favorable terms for your situation. Pay close attention to the variable rate index and margin used by the lender, as these factors will significantly impact your interest rate over time.

How to get a home equity line of credit

The procedure you need to follow to acquire a HELOC is similar to the process of purchasing or refinancing a mortgage. Here are the following documentation and demonstration you’ll need to follow when getting a HELOC:

- First of all, use the HELOC calculator to determine if you have enough equality.

- Once you find the estimated amount you can borrow, then you can look for HELOC lenders.

- Ensure you have the necessary documentation before applying.

- Once you have all the necessary, select the lender and apply.

Afterward, you can follow the instructions, where you will receive a disclosure document and you need to read them carefully. However, if you’re wondering how much I borrow, you need to under that the amount you can borrow from your home equity line of credit actually depends on the value of your home.

Utilizing HELOCs Responsibly

- Understand the terms: Carefully review your HELOC agreement and understand the interest rates, repayment terms, and fees.

- Borrow responsibly: Only borrow what you need and can afford to repay.

- Maintain timely payments: Late payments can lead to penalties and damage your credit score.

- Seek financial guidance: Consult a financial advisor to discuss your financial goals and determine if a HELOC aligns with your overall financial plan.

How to Choose a HELOC Lender

Here are some factors to consider when choosing a HELOC lender:

- Interest rates: Compare the interest rates offered by different lenders, paying close attention to the variable rate index and margin used to calculate the interest rate. Consider whether you prefer a fixed-rate HELOC or a variable-rate HELOC.

- Fees: Look for lenders with low or no fees, including annual fees, transaction fees, and early closure fees.

- Loan terms: Consider the length of the draw period and repayment period offered by different lenders. Choose a loan term that aligns with your financial goals and ability to repay the loan.

- Reputation and customer service: Research the lender’s reputation and customer service reviews to ensure a positive borrowing experience.

- Financial stability: Choose a lender with strong financial standing to ensure they can fulfill their obligations throughout the loan term.

- Accessibility and convenience: Consider the lender’s accessibility and convenience, such as online account management, mobile apps, and branch locations.

- Additional features: Some lenders may offer additional features, such as rate discounts for automatic payments or the ability to convert a variable-rate HELOC to a fixed-rate HELOC.

Tips for Managing a HELOC

Here are some tips for managing a Home Equity Line of Credit (HELOC) responsibly:

- Borrow only what you need: Avoid the temptation to borrow the entire available credit line. Only borrow the amount you need for your intended purpose.

- Make timely payments: Ensure you make your HELOC payments on time to avoid late fees and potential damage to your credit score. Consider setting up automatic payments to avoid missing deadlines.

- Understand the interest rate: HELOCs typically have variable interest rates, meaning they can fluctuate over time. Keep an eye on interest rate trends and understand how they can impact your monthly payments.

- Pay more than the minimum: Whenever possible, pay more than the minimum required payment to reduce the principal balance faster and save on interest costs over the long term.

- Have a repayment plan: Develop a clear repayment plan to ensure you can pay off the HELOC within the repayment period. Consider strategies like making extra payments or refinancing to manage the debt effectively.

- Avoid using HELOC for unnecessary expenses: It’s best to use a HELOC for significant investments or expenses that can improve your financial situation, such as home improvements, debt consolidation, or education. Avoid using it for discretionary spending or non-essential purchases.

- Monitor your credit utilization: Keep your credit utilization ratio low, ideally below 30% of your available credit. High credit utilization can negatively impact your credit score.

- Review your HELOC agreement: Familiarize yourself with the terms and conditions of your HELOC agreement, including interest rates, fees, repayment terms, and any potential penalties.

- Seek professional advice: If you have any questions or concerns about managing your HELOC, don’t hesitate to seek advice from a financial advisor or credit counselor.

By following these tips, you can effectively manage your HELOC and use it as a valuable financial tool without jeopardizing your financial well-being.

FAQs about HELOCs

How much can I borrow with a HELOC?

The amount you can borrow depends on your home equity, credit score, and lender’s policies. Typically, you can borrow up to 80-85% of your home equity.

What is the difference between a HELOC and a home equity loan?

A HELOC offers a revolving line of credit, while a home equity loan provides a lump sum upfront. HELOCs typically have variable interest rates, while home equity loans usually have fixed rates.

Are there any fees associated with a HELOC?

Some lenders may charge fees for application, appraisal, origination, or annual maintenance. Compare fee structures before choosing a lender.

Can I use a HELOC to buy another property?

Yes, you can use a HELOC for various purposes, including purchasing another property. However, ensure you have a solid repayment plan to avoid financial strain.

How do I repay a HELOC?

During the draw period, you may have the option to make interest-only payments. During the repayment period, you’ll repay the outstanding balance, including principal and interest, over a set term.

Can I convert my HELOC to a fixed-rate loan?

Some lenders offer the option to convert a portion or all of your HELOC balance to a fixed-rate loan, providing more predictable monthly payments.

Will a HELOC affect my credit score?

Applying for a HELOC may temporarily lower your credit score due to a hard inquiry. However, responsible management of the HELOC can positively impact your credit score over time.

Is a HELOC right for me?

A HELOC can be a valuable financial tool if used responsibly. Consider your financial needs, risk tolerance, and ability to repay the loan before deciding if a HELOC is the right choice for you.

Conclusion

HELOCs offer a valuable financial tool for homeowners seeking to access funds for various purposes. By understanding the features, benefits, and responsible use of HELOCs, homeowners can effectively harness their home equity and achieve their financial aspirations.